The Financial Impact of Caregiving A Guide to Protecting Your Money and Career

Practical modifications for safety and independence

The financial reality of caregiving is rarely discussed until you're living it. Between reduced work hours, increased expenses, and the hidden costs nobody mentions, caregiving can reshape your entire financial picture. This guide covers the real costs, practical strategies to minimize financial damage, and resources that can help. You're protecting your finances while providing good care. The system places the financial burden disproportionately on women who are already juggling careers and families. This is a structural problem that requires strategic planning to navigate.

About costs and timeline: Modification costs vary by complexity and location. Start with the most essential changes first and plan for professional installation of structural modifications.

1

The Real Costs of Caregiving

Medical and health costs insurance doesn't cover

Budget option

- Prescription copays and supplements: $50–200 monthly. - Medical equipment rentals: $75–300 monthly. - Home health aide services: $25–35 per hour. - Adult day programs: $78 average daily rate. - Transportation to appointments: $15–50 per trip.

Home modifications and safety equipment

Budget option

- Bathroom grab bars and shower seats: $100–500. - Ramps and stairlifts: $1,200–15,000. - Medical alert systems: $25–70 monthly. - Medication management systems: $30–150.

Daily living support

Budget option

- Grocery delivery fees: $5–15 per order. - Meal delivery services: $8–15 per meal. - Housekeeping services: $100–200 per visit. - Yard maintenance: $50–150 per visit. ### Hidden Financial Impacts

Lost income from reduced work hours

Budget option

The average family caregiver loses $324,044 in lifetime wages due to caregiving responsibilities. This includes missed promotions, reduced Social Security benefits, and gaps in retirement savings.

Increased personal expenses

Budget option

- Gas and mileage for frequent trips. - Phone bills from constant check-ins. - Your own healthcare costs from stress and delayed medical care. - Convenience foods and services when you're too exhausted to cook or clean.

Emergency fund depletion

Budget option

Caregiving creates ongoing financial unpredictability. Emergency funds get depleted by medical crises, equipment needs, and income fluctuations.

The Real Costs of Caregiving visual guide

2

Protecting Your Career and Income

Family and Medical Leave Act provides 12 weeks annually

Self-care strategy

FMLA provides up to 12 weeks of unpaid leave annually for caring for a family member with a serious health condition. You keep your health insurance and job protection during this time.

State family leave programs offer paid time

Self-care strategy

California, New Jersey, Rhode Island, New York, Washington, and Washington D.C. offer paid family leave. Benefits vary but typically provide partial wage replacement for 6–12 weeks. ### Negotiate Flexible Work Arrangements

Remote work options give you schedule control

Self-care strategy

Negotiate specific days or hours for remote work when your job allows it. Having control over your schedule reduces the need for emergency time off.

Compressed work weeks create appointment days

Self-care strategy

Working four 10-hour days instead of five 8-hour days gives you a full day for appointments and caregiving tasks.

Job sharing preserves benefits and career continuity

Self-care strategy

Some employers will restructure positions to retain experienced employees. This reduces your income but preserves benefits and career continuity.

Protecting Your Career and Income visual guide

3

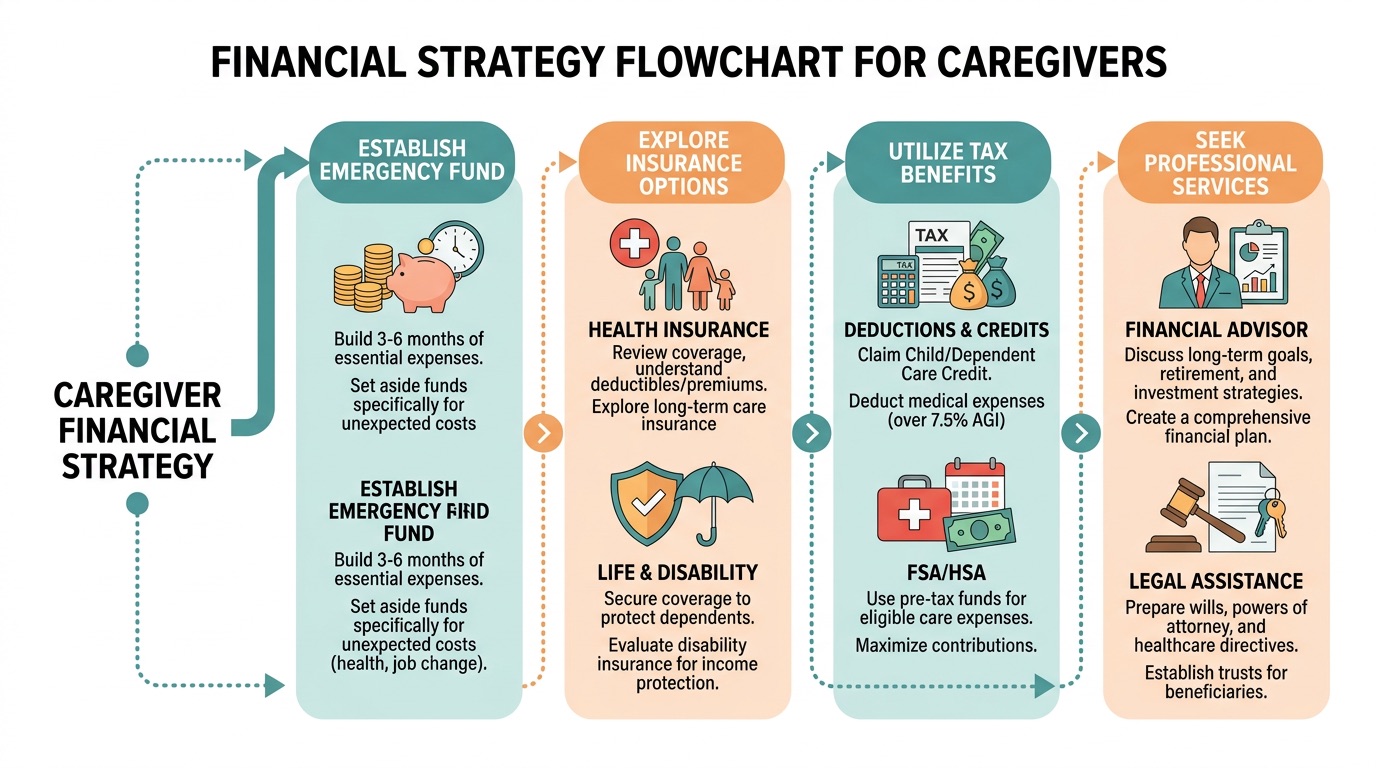

Financial Strategies That Work

Medicare and Medicaid cover specific services

Financial impact

Medicare covers some home health services, medical equipment, and therapy. Medicaid covers long-term care services that Medicare doesn't cover. Each program has specific eligibility requirements and covered services.

Veterans benefits provide monthly care payments

Financial impact

Veterans and their spouses may qualify for Aid and Attendance benefits, which provide monthly payments for care costs. The application process takes months, so start early.

Local Area Agency on Aging programs offer subsidized services

Financial impact

Most areas offer subsidized services like meal delivery, transportation, and respite care. Income limits vary by location and program. ### Plan for Tax Benefits

Medical expense deductions apply when costs exceed 7.5% of income

Financial impact

If your parent qualifies as your dependent, you can deduct medical expenses that exceed 7.5% of your adjusted gross income. This includes insurance premiums, medical equipment, and some home modifications.

Dependent care credit applies to adult day care

Financial impact

You may qualify for a tax credit for adult day care or respite care services that allow you to work.

Flexible Spending Accounts use pre-tax dollars

Financial impact

If your employer offers dependent care FSAs, you can use pre-tax dollars for qualifying caregiving expenses. ### Protect Your Retirement Savings

401(k) loans are better than early withdrawals

Financial impact

Early withdrawals trigger penalties and taxes. If you must access retirement funds, consider a 401(k) loan instead.

Small contributions maintain matching and habits

Financial impact

Even small contributions maintain the habit and capture any employer matching. Reduce the contribution percentage rather than stopping completely.

Spousal IRA contributions work when your income drops

Financial impact

If caregiving reduces your earned income, your working spouse can contribute to an IRA on your behalf.

Financial Strategies That Work visual guide

4

What You Can Do This Week

Key Tips

Start with the most important modifications first based on your current needs.

Consider both immediate safety and future accessibility when making changes.

Get multiple quotes from qualified contractors for major modifications.

Check with your insurance about coverage for medically necessary modifications.